1. Introduction to AI-Driven Insurance Pricing

Artificial Intelligence (AI) is transforming various industries, and insurance is no exception. AI-driven insurance pricing refers to the use of advanced algorithms and machine learning techniques to determine the premiums that policyholders should pay. This approach allows insurers to analyze vast amounts of data more efficiently and accurately than traditional methods.

- AI enhances risk assessment by evaluating numerous variables.

- It enables real-time pricing adjustments based on market conditions.

- Insurers can offer personalized premiums tailored to individual risk profiles.

1.1. What is AI-Powered Pricing in Insurance?

AI-powered pricing in insurance involves leveraging data analytics and machine learning to set insurance premiums. This method goes beyond traditional actuarial models by incorporating a wider range of data sources and predictive analytics.

- Utilizes big data: AI can analyze data from various sources, including social media, IoT devices, and historical claims data.

- Predictive modeling: Machine learning algorithms predict future risks based on past behaviors and trends.

- Dynamic pricing: Premiums can be adjusted in real-time based on changing risk factors or customer behavior.

AI-powered pricing aims to create a more accurate and fair pricing model, ensuring that customers pay premiums that reflect their actual risk levels. This approach can lead to better customer satisfaction and retention, ultimately driving greater ROI for insurers.

1.2. The Evolution of Insurance Pricing Models

Insurance pricing has evolved significantly over the years, moving from simplistic models to complex, data-driven approaches.

- Traditional models: Initially, insurance pricing relied heavily on basic statistical methods and historical data. Insurers used broad categories to assess risk, often leading to generalized pricing.

- Introduction of technology: The advent of computers allowed for more sophisticated calculations and the use of larger datasets. However, these methods still had limitations in terms of speed and adaptability.

- Rise of big data and AI: The integration of big data analytics and AI has revolutionized pricing models. Insurers can now process vast amounts of information quickly, leading to more precise risk assessments.

At Rapid Innovation, we harness the power of AI insurance pricing to help insurance companies optimize their pricing strategies, ensuring they remain competitive while maximizing profitability. The evolution of insurance pricing models reflects the industry's response to changing market dynamics and consumer expectations. As technology continues to advance, the trend towards AI-driven pricing is likely to grow, offering more personalized and fair insurance solutions.

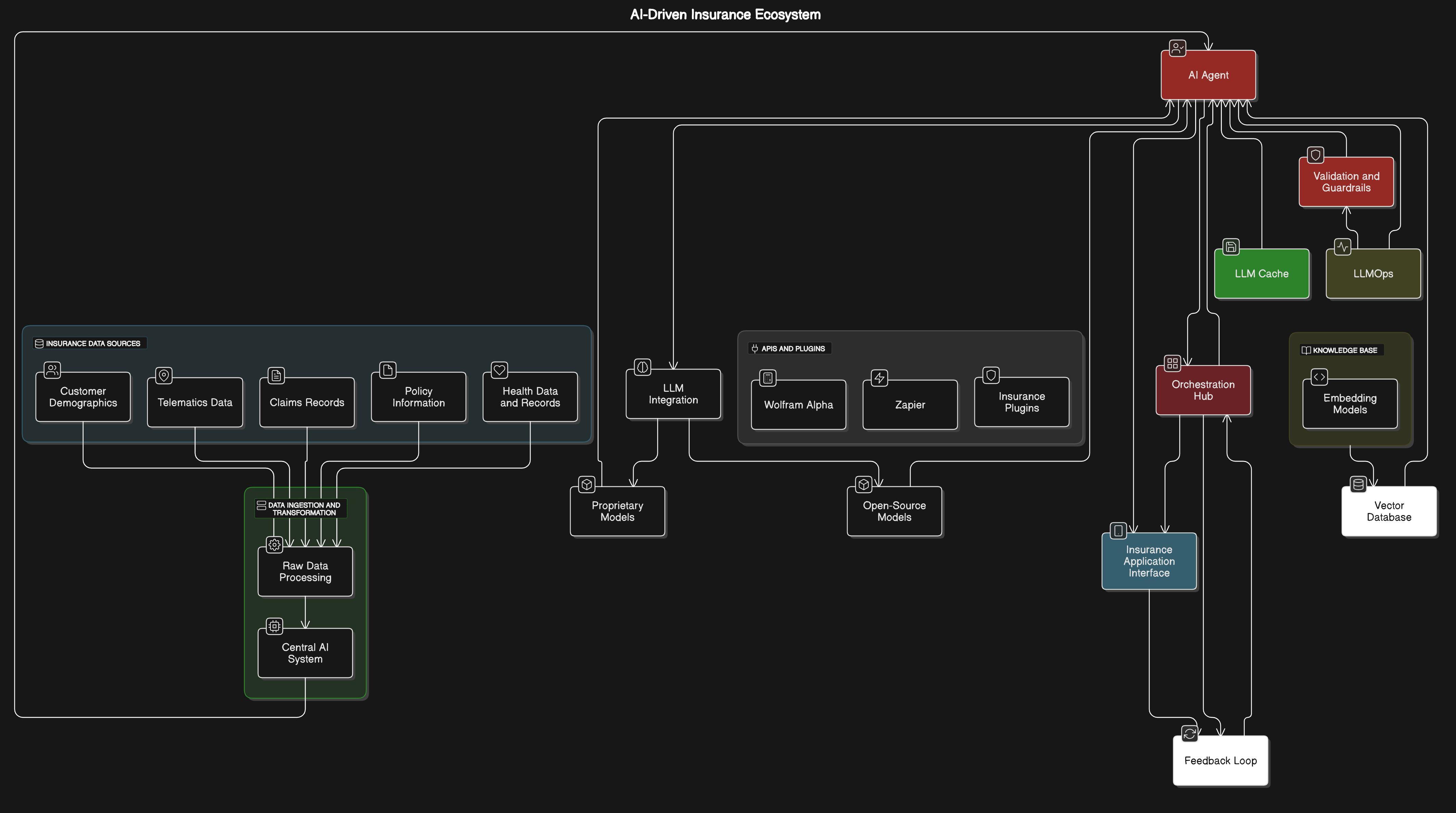

Refer to the image for a visual representation of AI-driven insurance pricing concepts:

1.3. Key Benefits of AI in Insurance Pricing

- Enhanced Accuracy: AI algorithms analyze vast amounts of data to provide more precise risk assessments, including those related to ai in insurance pricing. This leads to better pricing models that reflect the true risk associated with each policyholder, ultimately resulting in improved profitability for insurers.

- Improved Efficiency: Automation of data processing and analysis reduces the time required for underwriting and pricing decisions, particularly in the context of ai in insurance pricing. This efficiency allows insurers to respond more quickly to market changes and customer needs, enhancing their competitive edge.

- Personalized Pricing: AI enables insurers to create tailored pricing strategies based on individual customer profiles, which is a key aspect of ai in insurance pricing. This personalization can lead to higher customer satisfaction and loyalty, fostering long-term relationships and increasing retention rates.

- Fraud Detection: AI systems identify patterns indicative of fraudulent behavior, helping insurers mitigate risks and reduce losses. This capability not only protects the insurer's bottom line but also leads to more stable pricing for honest policyholders, a crucial benefit of ai in insurance pricing.

- Predictive Analytics: By leveraging historical data, AI can forecast future claims and losses, allowing insurers to adjust pricing proactively. This foresight helps maintain profitability while ensuring that insurers remain competitive in the marketplace, showcasing the impact of ai in insurance claims processing and pricing.

1.4. Impact on Customer Experience and Retention: Rapid Innovation’s AI Agent Solution for Dynamic Pricing Optimization

- Faster Response Times: AI-driven chatbots and virtual assistants provide immediate responses to customer inquiries, enhancing the overall customer experience. This quick access to information can lead to higher satisfaction rates and improved customer loyalty.

- Personalized Interactions: AI analyzes customer data to offer personalized recommendations and services. This tailored approach fosters a stronger connection between the insurer and the customer, enhancing engagement and satisfaction.

- Proactive Engagement: AI can identify potential issues before they escalate, allowing insurers to reach out to customers with solutions. This proactive approach can significantly improve customer retention and reduce churn.

- Streamlined Claims Process: AI technologies can automate claims processing, reducing the time it takes for customers to receive payouts. A smoother claims experience can lead to increased trust and loyalty among policyholders.

- Enhanced Communication: AI tools can facilitate better communication between insurers and customers, ensuring that policyholders are kept informed about their coverage and any changes. This transparency builds trust and encourages long-term relationships

.

At Rapid Innovation, we leverage AI agents to revolutionize insurance pricing by providing real-time, dynamic pricing adjustments tailored to individual customer behaviors and risk profiles. Our AI agents integrate with existing systems to process vast amounts of data, such as telematics, IoT sensors, and health metrics, ensuring that premiums are continuously optimized based on the latest information. This proactive pricing approach enhances customer experience by offering personalized rates, adjusting premiums dynamically in response to changes in risk factors, and improving retention through more competitive and fair pricing models. By utilizing AI-driven agents for predictive analytics and real-time adjustments, Rapid Innovation empowers insurers to remain agile, offering customers the best possible rates while maintaining profitability and compliance with industry regulations.

2. Use Cases of AI in Insurance Pricing

- Risk Assessment: Insurers use AI to analyze various data sources, including social media, telematics, and historical claims data, to assess risk more accurately. This helps in determining appropriate premiums for different customer segments, ultimately leading to better financial outcomes.

- Dynamic Pricing: AI enables insurers to implement dynamic pricing models that adjust premiums in real-time based on changing risk factors. This flexibility allows insurers to remain competitive in a rapidly evolving market, maximizing their revenue potential.

- Underwriting Automation: AI streamlines the underwriting process by automating data collection and analysis. This reduces the workload for underwriters and speeds up the decision-making process, allowing insurers to serve customers more efficiently.

- Customer Segmentation: AI can identify distinct customer segments based on behavior and preferences. This segmentation allows insurers to tailor their pricing strategies and marketing efforts more effectively, enhancing their overall market positioning.

- Claims Prediction: AI models can predict the likelihood of claims based on various factors, enabling insurers to adjust pricing accordingly. This predictive capability helps in managing risk and maintaining profitability, ensuring sustainable growth for the insurer.

Refer to the image for a visual representation of the key benefits of AI in insurance pricing.

2.1. Auto Insurance

Auto insurance is a crucial aspect of vehicle ownership, providing financial protection against accidents, theft, and other damages. The industry has evolved significantly, incorporating technology and data analytics to enhance customer experience and improve risk assessment. It provides coverage for liability, collision, and comprehensive damages, and is required by law in most states to protect drivers and other road users. Premiums are determined based on various factors, including driving history, vehicle type, and location.

2.1.1. Telematics and Usage-Based Pricing

Telematics refers to the integration of telecommunications and monitoring systems in vehicles, allowing insurers to collect data on driving behavior. Usage-based pricing (UBP) leverages this data to determine insurance premiums based on actual driving habits rather than traditional metrics. This system collects data on speed, braking patterns, acceleration, and mileage, offers personalized premiums based on individual driving behavior, and encourages safer driving habits through feedback and rewards.

Telematics can lead to significant savings for safe drivers. According to a study, drivers who adopt telematics car insurance can save up to 30% on their premiums. This technology also helps insurers better assess risk, leading to more accurate pricing models. Insurers can identify high-risk drivers and adjust premiums accordingly, provide real-time data that can expedite claims processing, and enhance customer engagement through mobile apps and dashboards.

At Rapid Innovation, we leverage AI algorithms to analyze telematics data, enabling insurers to create dynamic pricing models that reflect real-time driving behavior. Our solutions help clients achieve greater ROI by optimizing their pricing strategies and reducing claims costs through improved risk assessment.

2.1.2. Driver Behavior Analysis

Driver behavior analysis involves evaluating how individuals operate their vehicles to assess risk and tailor insurance products. This analysis is often conducted through telematics data but can also include other methods such as surveys and driving simulations. It focuses on key metrics like speed, braking, cornering, and distraction levels, helps insurers identify patterns that correlate with higher accident rates, and enables targeted interventions, such as driver training programs.

By understanding driver behavior, insurers can create more personalized insurance products. For instance, drivers who demonstrate safe habits may qualify for discounts or rewards, while those with risky behaviors may face higher premiums. This approach promotes safer driving through incentives and feedback, can lead to a reduction in accident rates and claims, and supports the development of new insurance models, such as pay-per-mile or pay-as-you-drive.

Rapid Innovation employs advanced AI techniques to analyze driver behavior data, allowing insurers to implement targeted interventions that enhance safety and reduce risk. Our expertise in AI-driven analytics empowers clients to refine their product offerings, ultimately leading to increased customer satisfaction and loyalty.

Driver behavior analysis not only benefits insurers but also enhances road safety. Studies have shown that telematics programs can reduce crash rates by up to 15% among participating drivers. This creates a win-win situation for both insurers and policyholders. Additionally, the rise of auto insurance tech companies is further driving innovation in the sector, with solutions that include non telematics car insurance options and advancements in auto tech insurance. As the industry continues to evolve, understanding the meaning of telematics car insurance and its implications will be essential for both insurers and consumers. For more insights on driver monitoring systems.

2.1.3. Real-Time Risk Adjustment

Real-time risk adjustment refers to the dynamic assessment and modification of risk profiles based on current data and conditions. This approach is increasingly utilized in various sectors, particularly in insurance and finance.

- Continuous data monitoring: Insurers can track real-time data from various sources, such as telematics, weather reports, and market trends. Rapid Innovation leverages AI algorithms to analyze this data, enabling insurers to make informed decisions swiftly.

- Adaptive pricing models: Premiums can be adjusted based on the current risk level, allowing for more accurate pricing that reflects the actual risk exposure. Our blockchain solutions can ensure transparency and security in these pricing adjustments, fostering trust between insurers and policyholders.

- Enhanced customer engagement: Policyholders receive immediate feedback on their risk status, which can encourage safer behaviors and reduce claims. By integrating AI-driven insights, Rapid Innovation helps insurers create personalized communication strategies that enhance customer relationships.

- Improved underwriting processes: Real-time data allows for more precise risk assessments, leading to better-informed underwriting decisions. Our AI tools streamline the underwriting process, reducing time and costs while increasing accuracy.

- Regulatory compliance: Insurers can ensure they meet regulatory requirements by continuously updating risk assessments based on real-time data. Rapid Innovation's solutions help automate compliance checks, minimizing the risk of non-compliance. For more information on how we can assist with AI-driven solutions in insurance, visit our AI-driven solutions in insurance.

2.1.4. Connected Vehicle Data Integration

Connected vehicle data integration involves the use of data collected from vehicles equipped with internet connectivity and sensors. This data can provide valuable insights for various applications, including insurance, traffic management, and vehicle maintenance.

- Data sources: Connected vehicles generate data on driving behavior, vehicle performance, and environmental conditions. Rapid Innovation utilizes AI to analyze this data, providing insurers with actionable insights for risk assessment.

- Enhanced risk assessment: Insurers can analyze driving patterns to better understand risk profiles and tailor policies accordingly. Our advanced analytics tools enable insurers to create more personalized and competitive offerings.

- Accident prevention: Real-time data can help identify hazardous conditions and alert drivers, potentially reducing accidents. Rapid Innovation's AI solutions can facilitate the development of predictive models that enhance driver safety.

- Fleet management: Businesses can optimize their fleet operations by monitoring vehicle health and driver behavior, leading to cost savings. Our blockchain technology ensures secure and efficient data sharing among fleet operators, enhancing operational efficiency.

- Collaboration opportunities: Automakers, insurers, and tech companies can work together to develop innovative solutions that leverage connected vehicle data. Rapid Innovation fosters partnerships that drive innovation in the connected vehicle ecosystem.

2.2. Property Insurance

Property insurance is a type of coverage that protects individuals and businesses from financial losses due to damage or loss of property. This insurance can cover various types of property, including homes, commercial buildings, and personal belongings.

- Coverage types: Property insurance can include homeowners insurance, renters insurance, and commercial property insurance, each tailored to specific needs. Rapid Innovation assists insurers in developing customized products that meet diverse customer requirements.

- Risk assessment: Insurers evaluate the risk associated with a property based on factors such as location, construction type, and historical claims data. Our AI-driven analytics enhance the accuracy of these assessments, leading to better pricing strategies.

- Claims process: In the event of a loss, policyholders must file a claim, which is then assessed by the insurer to determine the payout. Rapid Innovation streamlines the claims process through automation, improving efficiency and customer satisfaction.

- Premium factors: Premiums are influenced by various factors, including the property's value, coverage limits, and the policyholder's claims history. Our solutions provide insurers with the tools to analyze these factors comprehensively, ensuring competitive pricing.

- Emerging trends: The property insurance industry is evolving with advancements in technology, such as the use of drones for property assessments and AI for claims processing. Rapid Innovation is at the forefront of these trends, helping clients adopt cutting-edge technologies to enhance their operations.

Refer to the image for a visual representation of real-time risk adjustment and its components.

2.2.1. Geospatial and Environmental Risk Assessment

Geospatial and environmental risk assessment involves analyzing spatial data to identify potential risks associated with environmental factors. This process is crucial for various industries, including insurance, urban planning, and disaster management. Rapid Innovation leverages advanced AI algorithms and blockchain technology to enhance the accuracy and reliability of these assessments.

- Utilizes Geographic Information Systems (GIS) to map and analyze data, ensuring precise risk identification.

- Identifies areas prone to natural disasters such as floods, earthquakes, and wildfires, allowing businesses to strategize effectively.

- Assesses environmental factors like air quality, soil stability, and water resources, providing a comprehensive view of potential risks.

- Helps in making informed decisions regarding land use and development, optimizing resource allocation.

- Supports risk mitigation strategies by providing insights into vulnerable regions, enhancing overall safety.

- Enhances emergency preparedness by predicting the impact of environmental hazards, thus reducing response times.

- Integrates data from multiple sources, including satellite imagery and historical records, ensuring a holistic approach to risk assessment.

- Incorporates environmental risk assessment methodologies such as environmental health risk assessment and ecological risk assessment to evaluate potential impacts on ecosystems and human health.

- Utilizes tools like the environmental risk assessment matrix to systematically analyze and prioritize risks.

- Conducts epa risk assessment and epa human health risk assessment to comply with regulatory standards and ensure public safety.

2.2.2. Weather Pattern Analysis for Premiums

Weather pattern analysis is essential for determining insurance premiums, especially in sectors like property and agriculture. By understanding weather trends, insurers can better assess risk and set appropriate pricing. Rapid Innovation employs AI-driven analytics to refine this process, leading to improved ROI for our clients.

- Analyzes historical weather data to identify trends and anomalies, enabling more accurate risk assessments.

- Considers factors such as temperature fluctuations, precipitation levels, and storm frequency, ensuring comprehensive coverage.

- Helps insurers predict potential claims based on weather-related events, reducing unexpected losses.

- Allows for the development of tailored insurance products that reflect specific risks, enhancing customer satisfaction.

- Supports dynamic pricing models that adjust premiums based on real-time weather data, optimizing profitability.

- Enhances customer trust by providing transparent pricing based on empirical data, fostering long-term relationships.

- Facilitates better risk management strategies for both insurers and policyholders, ultimately driving greater ROI.

- Incorporates sustainability risk assessment to evaluate the long-term impacts of weather patterns on insured properties.

2.2.3. IoT Data for Property Risk Monitoring

The Internet of Things (IoT) has revolutionized property risk monitoring by providing real-time data from connected devices. This technology enhances the ability to assess and manage risks associated with properties. Rapid Innovation integrates IoT solutions with AI analytics to deliver actionable insights for our clients.

- Utilizes sensors and smart devices to collect data on environmental conditions, ensuring continuous monitoring.

- Monitors factors such as temperature, humidity, and water leaks in real-time, enabling proactive risk management.

- Enables proactive risk management by alerting property owners to potential issues, minimizing damage and loss.

- Reduces response times to incidents, ensuring swift action and preserving asset value.

- Supports data-driven decision-making for maintenance and insurance claims, enhancing operational efficiency.

- Enhances the accuracy of risk assessments by providing continuous data streams, leading to better-informed strategies.

- Encourages the development of smart insurance products that leverage IoT data for personalized coverage, driving innovation in the insurance sector.

- Integrates environmental exposure assessment data to better understand the risks associated with property locations.

Through these advanced methodologies, Rapid Innovation empowers clients to achieve their business goals efficiently and effectively, ultimately leading to greater ROI.

2.2.4. Claims Prevention through Predictive Maintenance

Predictive maintenance is a proactive approach that uses data analysis to predict when equipment failure might occur. This strategy is increasingly being adopted in various industries, including predictive maintenance in healthcare, to prevent claims and reduce costs.

- Data Utilization: Predictive maintenance relies on data collected from equipment sensors, historical performance, and maintenance records. This data helps identify patterns that indicate potential failures, allowing organizations to leverage AI-driven analytics for more accurate predictions.

- Cost Reduction: By anticipating equipment failures, organizations can schedule maintenance before issues arise, reducing the likelihood of costly emergency repairs and associated claims. Rapid Innovation's expertise in AI can help clients implement systems that optimize maintenance schedules, leading to significant cost savings.

- Improved Equipment Lifespan: Regular maintenance based on predictive analytics can extend the lifespan of equipment, leading to fewer replacements and lower overall costs. Our solutions can integrate blockchain technology to ensure transparent and tamper-proof maintenance records, enhancing accountability.

- Enhanced Patient Safety: In healthcare, ensuring that medical equipment is functioning optimally is crucial for patient safety. Predictive maintenance helps prevent equipment malfunctions that could lead to adverse patient outcomes, thereby improving the quality of care.

- Operational Efficiency: Organizations can optimize their maintenance schedules, reducing downtime and improving overall operational efficiency. This can lead to better service delivery and patient satisfaction, ultimately contributing to a higher return on investment (ROI).

2.3. Health Insurance

Health insurance is a critical component of the healthcare system, providing financial protection against medical expenses. It plays a significant role in ensuring access to necessary healthcare services.

- Types of Coverage: Health insurance can be categorized into various types, including employer-sponsored plans, government programs (like Medicare and Medicaid), and individual plans.

- Cost Management: Health insurance helps manage the high costs of medical care, allowing individuals to receive necessary treatments without facing overwhelming financial burdens.

- Preventive Services: Many health insurance plans cover preventive services at no additional cost, encouraging individuals to seek regular check-ups and screenings to catch health issues early.

- Access to Care: Health insurance increases access to healthcare services, ensuring that individuals can receive timely medical attention when needed.

- Risk Pooling: By pooling resources from many individuals, health insurance spreads the financial risk associated with healthcare costs, making it more manageable for everyone involved.

2.3.1. Health Risk Scoring and Wellness Data

Health risk scoring is a method used by health insurers and providers to assess an individual's health risks based on various factors. This scoring can inform personalized care plans and wellness initiatives.

- Data Collection: Health risk scoring typically involves collecting data from medical history, lifestyle choices, and biometric screenings. This data helps create a comprehensive picture of an individual's health.

- Risk Stratification: Individuals are categorized into different risk levels (low, moderate, high) based on their health risk scores. This stratification allows for targeted interventions.

- Personalized Interventions: High-risk individuals may receive tailored wellness programs, such as chronic disease management or lifestyle coaching, to help mitigate their health risks.

- Incentives for Healthy Behavior: Many health insurance plans offer incentives for individuals to engage in healthy behaviors, such as regular exercise, smoking cessation, and routine health screenings.

- Improved Outcomes: By utilizing health risk scoring and wellness data, insurers and providers can improve health outcomes, reduce healthcare costs, and enhance the overall quality of care. Rapid Innovation can assist in developing AI-driven platforms that analyze this data effectively, leading to better decision-making and improved ROI for healthcare organizations.

2.3.2. Predictive Models for Chronic Conditions

Predictive models for chronic conditions utilize data analytics and machine learning to forecast the likelihood of developing specific health issues. These models are essential in healthcare for several reasons:

- Data Utilization: They analyze vast amounts of patient data, including demographics, medical history, lifestyle choices, and genetic information.

- Risk Stratification: By identifying high-risk patients, healthcare providers can allocate resources more effectively and prioritize interventions.

- Early Intervention: Predictive models enable early detection of potential health issues, allowing for timely preventive measures that can improve patient outcomes.

- Cost Reduction: By preventing the progression of chronic diseases, these predictive models for chronic conditions can significantly reduce healthcare costs associated with hospitalizations and long-term treatments.

- Continuous Learning: As more data becomes available, predictive models can be refined and improved, leading to better accuracy and reliability over time.

These models are increasingly being integrated into electronic health records (EHRs) and decision support systems, enhancing the ability of healthcare providers to make informed decisions. At Rapid Innovation, we leverage our expertise in AI to develop tailored predictive models for chronic conditions that empower healthcare organizations to enhance patient care and achieve greater ROI through improved resource allocation and reduced costs.

2.3.3. Personalized Preventive Care Incentives

Personalized preventive care incentives are tailored strategies designed to encourage individuals to engage in health-promoting behaviors. These incentives can take various forms:

- Financial Incentives: Offering discounts on insurance premiums or cash rewards for completing preventive screenings and maintaining healthy lifestyles.

- Customized Health Plans: Developing personalized health plans based on individual risk factors, preferences, and health goals, which can motivate patients to participate actively in their care.

- Access to Resources: Providing access to wellness programs, fitness classes, and nutritional counseling that align with individual needs and interests.

- Behavioral Nudges: Implementing reminders and motivational messages that encourage individuals to take preventive actions, such as scheduling regular check-ups or vaccinations.

- Community Engagement: Creating community-based initiatives that foster social support and accountability, making it easier for individuals to adopt healthier behaviors.

These personalized approaches not only improve individual health outcomes but also enhance overall population health by reducing the incidence of preventable diseases. Rapid Innovation can assist organizations in designing and implementing these incentive programs using AI-driven insights to maximize engagement and effectiveness.

2.3.4. Lifestyle-Based Premium Adjustments

Lifestyle-based premium adjustments are a strategy used by insurance companies to modify health insurance premiums based on an individual's lifestyle choices. This approach has several implications:

- Incentivizing Healthy Behaviors: Individuals who engage in healthy behaviors, such as regular exercise, balanced nutrition, and smoking cessation, may receive lower premiums as a reward for their commitment to health.

- Data-Driven Assessments: Insurers often use data from health assessments, wearable devices, and health screenings to evaluate lifestyle choices and determine premium adjustments.

- Encouraging Preventive Care: By linking premiums to lifestyle factors, insurers encourage policyholders to participate in preventive care measures, which can lead to better health outcomes and lower costs.

- Potential Disparities: There are concerns that lifestyle-based premium adjustments may disproportionately affect individuals with limited access to resources or those facing socioeconomic challenges, leading to inequities in healthcare.

- Regulatory Considerations: Insurance companies must navigate regulations that govern how they can adjust premiums based on lifestyle factors, ensuring compliance with laws designed to protect consumers.

Overall, lifestyle-based premium adjustments aim to create a healthier population while promoting personal responsibility for health outcomes. Rapid Innovation's expertise in blockchain technology can also enhance transparency and trust in these premium adjustment processes, ensuring that data is securely managed and accessible for all stakeholders involved.

2.4. Life Insurance

Life insurance is a financial product that provides a monetary benefit to beneficiaries upon the death of the insured individual. It serves as a safety net for families, ensuring financial stability in the event of an untimely death. The life insurance industry relies heavily on various models and analyses to assess life insurance risk assessment and determine premiums. It provides financial security for dependents, helps cover debts and living expenses, and can be used as an investment vehicle in some cases.

2.4.1. Mortality Risk Models

Mortality risk models are statistical tools used by life insurance companies to predict the likelihood of death within a specific population. These models help insurers determine premiums and assess the risk associated with insuring an individual.

- Types of Mortality Risk Models:

- Actuarial Models: Use historical data to estimate life expectancy and mortality rates.

- Predictive Analytics: Incorporate machine learning and big data to refine risk assessments, enabling insurers to make data-driven decisions that enhance profitability.

- Cohort Studies: Analyze specific groups over time to identify trends in mortality, allowing for targeted product offerings.

- Key Factors Considered:

- Age: Older individuals typically have higher mortality rates.

- Gender: Women generally have longer life expectancies than men.

- Health Status: Pre-existing conditions can significantly increase risk.

- Lifestyle Choices: Smoking, alcohol consumption, and physical activity levels are critical indicators.

- Importance of Mortality Risk Models:

- Helps insurers set appropriate premiums based on individual risk profiles, leading to improved customer satisfaction and retention.

- Aids in the development of new insurance products tailored to specific demographics, enhancing market competitiveness.

- Enhances the overall sustainability of the insurance pool by balancing risk, ultimately contributing to greater ROI for insurers.

2.4.2. Lifestyle and Genetic Factor Analysis

Lifestyle and genetic factor analysis plays a crucial role in assessing an individual's risk profile for life insurance. Insurers evaluate both lifestyle choices and genetic predispositions to better understand potential health risks.

- Lifestyle Factors:

- Diet and Nutrition: Poor dietary habits can lead to chronic diseases, affecting life expectancy.

- Physical Activity: Regular exercise is linked to lower mortality rates.

- Substance Use: Smoking and excessive alcohol consumption are significant risk factors.

- Stress Management: High-stress levels can lead to various health issues, impacting longevity.

- Genetic Factors:

- Family History: A family history of certain diseases (e.g., heart disease, cancer) can indicate higher risk.

- Genetic Testing: Some insurers may offer discounts for individuals who undergo genetic testing and demonstrate low-risk profiles, fostering a proactive approach to health management.

- Hereditary Conditions: Conditions like Huntington's disease or certain types of diabetes can significantly influence mortality risk.

- Impact on Insurance Premiums:

- Individuals with healthier lifestyles may qualify for lower premiums, incentivizing positive behavior changes.

- Genetic predispositions can lead to higher premiums or exclusions for certain conditions, allowing for more accurate risk assessment.

- Insurers are increasingly using this data to create personalized insurance plans, enhancing customer engagement and loyalty.

- Emerging Trends:

- Use of wearable technology to monitor health metrics, providing real-time data for insurers to refine risk models.

- Integration of telemedicine and health apps to promote healthier lifestyles, aligning with the growing trend of digital health solutions.

- Growing acceptance of genetic information in underwriting processes, paving the way for innovative insurance products.

Understanding mortality risk models and lifestyle and genetic factor analysis is essential for both insurers and policyholders. These tools not only help in determining premiums but also encourage healthier living, ultimately benefiting society as a whole. At Rapid Innovation, we leverage AI and blockchain technologies to enhance these processes, ensuring that our clients achieve greater ROI through efficient life insurance risk assessment and personalized insurance solutions. For more information on our services, visit our AI insurance solutions and learn more about technology and AI-based insurance solutions.

2.4.3. Predictive Models for Longevity

Predictive models for longevity are statistical tools that analyze various factors to estimate an individual's lifespan. These models leverage historical data and advanced algorithms to provide insights into life expectancy.

- Factors considered in predictive models:

- Age, gender, and ethnicity

- Lifestyle choices: (e.g., smoking, diet, exercise)

- Medical history and pre-existing conditions

- Socioeconomic status and education level

- Environmental influences: (e.g., pollution, access to healthcare)

- Types of predictive models:

- Actuarial models: Use historical mortality data to predict future life expectancy.

- Machine learning models: Employ algorithms to identify patterns in large datasets, improving accuracy over traditional methods.

- Survival analysis: Focuses on time-to-event data, estimating the duration until a specific event occurs, such as death.

- Applications in insurance:

- Tailoring life insurance premiums based on individual risk profiles, allowing insurers to offer more competitive rates.

- Enhancing underwriting processes by providing more accurate assessments of longevity, which can lead to better risk management.

- Informing product development by identifying trends in longevity and health, enabling insurers to create products that meet evolving customer needs.

- Challenges:

- Data privacy concerns when using personal health information, necessitating robust data protection measures.

- The need for continuous model updates to reflect changing health trends and advancements in medicine, ensuring that predictions remain relevant.

2.4.4. Family History and Health Data Integration

Integrating family history and health data is crucial for understanding an individual's health risks and potential longevity. This integration allows for a more comprehensive view of health factors that may influence life expectancy.

- Importance of family history:

- Genetic predispositions: Certain diseases may run in families, increasing the likelihood of similar health issues.

- Behavioral patterns: Family habits regarding diet, exercise, and lifestyle can impact health outcomes.

- Early detection: Knowledge of family health history can lead to proactive health screenings and interventions.

- Health data integration:

- Electronic health records (EHRs): Centralized databases that compile patient health information, including family history, facilitating better risk assessment.

- Wearable technology: Devices that track health metrics, providing real-time data that can be correlated with family health trends, enhancing predictive capabilities.

- Genetic testing: Offers insights into hereditary conditions, allowing for personalized health management and targeted interventions.

- Benefits of integration:

- Improved risk assessment: More accurate predictions of health risks based on comprehensive data, leading to better underwriting decisions.

- Enhanced preventive care: Identifying at-risk individuals can lead to targeted interventions and lifestyle changes, ultimately reducing healthcare costs.

- Better communication: Facilitates discussions between patients and healthcare providers about family health history and its implications, fostering a proactive approach to health management.

- Challenges:

- Data interoperability: Ensuring different health systems can share and interpret data effectively, which is essential for comprehensive risk assessment.

- Privacy concerns: Safeguarding sensitive family health information while integrating data, requiring adherence to strict data protection regulations.

3. Core AI Technologies in Insurance Premium Calculation

AI technologies are transforming the way insurance premiums are calculated, making the process more efficient and accurate. These technologies analyze vast amounts of data to assess risk and determine appropriate pricing.

- Key AI technologies used:

- Machine learning: Algorithms that learn from data patterns to predict outcomes, such as the likelihood of claims, enhancing the accuracy of risk assessments.

- Natural language processing (NLP): Analyzes unstructured data, such as customer feedback and claims reports, to extract valuable insights that inform underwriting decisions.

- Predictive analytics: Uses historical data to forecast future events, helping insurers anticipate risks and adjust premiums accordingly.

- Benefits of AI in premium calculation:

- Enhanced accuracy: AI models can process complex datasets, leading to more precise risk assessments and better pricing strategies.

- Real-time data analysis: Insurers can adjust premiums dynamically based on current data, improving competitiveness and responsiveness to market changes.

- Cost efficiency: Automating data analysis reduces the time and resources needed for premium calculations, allowing insurers to allocate resources more effectively.

- Applications in the insurance industry:

- Personalized pricing: Tailoring premiums based on individual risk factors, leading to fairer pricing models that reflect actual risk.

- Fraud detection: Identifying suspicious claims through pattern recognition and anomaly detection, reducing losses and improving profitability.

- Customer segmentation: Classifying customers based on risk profiles to optimize marketing strategies and improve customer targeting.

- Challenges:

- Data quality: Ensuring the accuracy and completeness of data used in AI models, which is critical for reliable predictions.

- Regulatory compliance: Navigating legal frameworks governing data use and privacy in insurance, ensuring adherence to industry standards.

- Ethical considerations: Addressing biases in AI algorithms that may lead to unfair pricing practices, promoting fairness and transparency in the insurance process.

At Rapid Innovation, we leverage our expertise in AI and blockchain technologies to help clients navigate these challenges, ensuring they achieve greater ROI through enhanced decision-making, improved risk management, and innovative product offerings.

3.1. Machine Learning for Risk Assessment

Machine learning (ML) has transformed the landscape of risk assessment across various industries, particularly in finance, insurance, and healthcare. By leveraging vast amounts of data, ML algorithms can identify patterns and predict outcomes, enabling organizations to make informed decisions regarding risk management. The key benefits of ML in risk assessment include:

- Enhances accuracy in risk evaluation.

- Automates data analysis processes.

- Adapts to new data and evolving risk factors.

3.1.1. Predictive Analytics in Premium Setting

Predictive analytics utilizes historical data and statistical algorithms to forecast future events. In the context of premium setting, it helps insurers determine the appropriate premiums for policyholders based on their risk profiles. This process involves analyzing historical claims data to identify trends, considering various factors such as age, health, and lifestyle, and utilizing algorithms to predict the likelihood of future claims.

The benefits of predictive analytics in premium setting include:

- Improved pricing accuracy, leading to fairer premiums.

- Enhanced customer segmentation for targeted marketing.

- Increased competitiveness in the insurance market.

For instance, a study found that predictive analytics can reduce underwriting costs by up to 30%. At Rapid Innovation, we leverage our expertise in machine learning for risk analysis to help clients implement AI-powered predictive analytics solutions for insurance that drive efficiency and profitability.

3.1.2. Real-Time Risk Scoring Algorithms

Real-time risk scoring algorithms assess the risk associated with a particular individual or entity at the moment of decision-making. These algorithms continuously analyze incoming data to provide up-to-date risk assessments. They incorporate real-time data from various sources, such as social media and transaction history, adjust risk scores dynamically based on new information, and enable immediate decision-making for underwriting and claims processing.

Key advantages of real-time risk scoring include:

- Faster response times in underwriting processes.

- Enhanced fraud detection capabilities.

- Improved customer experience through personalized offerings.

Research indicates that organizations using real-time risk scoring can achieve a 20% reduction in fraud losses. Rapid Innovation assists clients in integrating these advanced algorithms into their systems, ensuring they remain competitive and responsive to market changes.

By integrating machine learning into risk assessment, organizations can not only enhance their operational efficiency but also provide better services to their customers. This includes credit risk analysis using machine learning and risk assessment using machine learning. At Rapid Innovation, we are committed to helping our clients harness the power of AI to achieve greater ROI and drive business success.

3.1.3. Behavioral Pricing Models

Behavioral pricing models focus on understanding how consumers perceive prices and make purchasing decisions. These models take into account psychological factors that influence buying behavior, rather than relying solely on traditional economic theories, such as a behavioral approach to asset pricing.

- Price perception: Consumers often do not evaluate prices in absolute terms but rather in relative terms. For example, a price may seem more attractive if it is framed as a discount from a higher original price.

- Anchoring effect: The initial price presented can serve as an anchor, influencing how consumers perceive subsequent prices. This can lead to a higher willingness to pay if the initial price is set strategically.

- Reference pricing: Consumers often compare prices to a reference point, which can be the price of a similar product or the price they have paid in the past. This can affect their perception of value.

- Price sensitivity: Different consumer segments exhibit varying levels of price sensitivity. Understanding these segments can help businesses tailor their pricing strategies effectively.

- Behavioral biases: Factors such as loss aversion, where consumers prefer to avoid losses rather than acquire equivalent gains, can significantly impact pricing strategies, which is a key consideration in behavioral pricing models.

3.2. Deep Learning in Pricing Models

Deep learning has emerged as a powerful tool in developing pricing models, leveraging vast amounts of data to uncover complex patterns and insights that traditional methods may overlook.

- Data-driven insights: Deep learning algorithms can analyze large datasets, identifying trends and correlations that inform pricing strategies.

- Dynamic pricing: By continuously learning from market conditions and consumer behavior, deep learning models can adjust prices in real-time to optimize revenue.

- Predictive analytics: These models can forecast demand and price elasticity, allowing businesses to set prices that maximize profitability while remaining competitive.

- Customer segmentation: Deep learning can help identify distinct customer segments based on purchasing behavior, enabling personalized pricing strategies.

- Enhanced accuracy: The ability of deep learning models to process unstructured data, such as customer reviews and social media sentiment, enhances the accuracy of pricing decisions.

3.2.1. Neural Networks for Complex Pattern Analysis

Neural networks are a subset of deep learning that excel in recognizing complex patterns within data, making them particularly useful for pricing models.

- Structure: Neural networks consist of interconnected layers of nodes (neurons) that process input data and learn from it through training.

- Non-linear relationships: They can capture non-linear relationships between variables, which is crucial for understanding the complexities of consumer behavior and pricing dynamics.

- Feature extraction: Neural networks automatically identify relevant features from raw data, reducing the need for manual feature engineering and allowing for more nuanced analysis.

- Training on historical data: By training on historical sales data, neural networks can learn patterns that inform future pricing strategies, adapting to changes in consumer behavior over time.

- Applications: Neural networks can be applied in various pricing scenarios, including demand forecasting, price optimization, and competitive pricing analysis, which can be enhanced by incorporating behavioral pricing models.

Incorporating behavioral pricing models with deep learning techniques, particularly neural networks, can lead to more effective pricing strategies that align with consumer behavior and market dynamics. At Rapid Innovation, we leverage these advanced methodologies to help our clients optimize their pricing strategies, ultimately driving greater ROI and enhancing their competitive edge in the market. By integrating AI and deep learning into pricing models, we empower businesses to make data-driven decisions that resonate with consumer psychology, ensuring they achieve their business goals efficiently and effectively.

3.2.2. NLP for Underwriting and Risk Factors

Natural Language Processing (NLP) is transforming the underwriting process in the insurance industry by enabling better risk assessment and decision-making.

- Enhanced Data Extraction: NLP algorithms can analyze unstructured data from various sources, such as social media, news articles, and customer reviews. This helps underwriters identify potential risks associated with a policyholder or a property, ultimately leading to more informed underwriting decisions. Applications of nlp in insurance are becoming increasingly prevalent as companies seek to harness this technology.

- Improved Risk Assessment: By processing large volumes of text data, NLP can uncover hidden patterns and trends that may indicate higher risk. For example, sentiment analysis can gauge public perception of a particular area, which may influence property values and risk levels, allowing insurers to adjust their strategies accordingly. The exploration of nlp use cases in insurance is vital for enhancing risk assessment methodologies.

- Automation of Underwriting Processes: NLP can automate routine tasks, such as data entry and document review, allowing underwriters to focus on more complex cases. This leads to faster decision-making and improved efficiency in the underwriting process, enhancing overall productivity and reducing operational costs. The integration of nlp in the insurance industry is streamlining these processes significantly.

- Regulatory Compliance: NLP tools can help ensure compliance with regulations by monitoring communications and flagging any potential issues. This reduces the risk of legal complications and enhances the overall integrity of the underwriting process, safeguarding the organization’s reputation. The role of natural language processing in insurance compliance is becoming increasingly critical.

At Rapid Innovation, we leverage these advanced technologies to empower our clients in the insurance sector, enabling them to achieve greater ROI through enhanced efficiency, accuracy, and strategic foresight. Our expertise in AI and blockchain solutions ensures that your organization can navigate the complexities of the insurance landscape with confidence, particularly in areas like nlp in insurance industry and neuro linguistic programming insurance.

4. Data-Driven Premium Optimization

Data-driven premium optimization refers to the use of advanced analytics and big data to determine the most accurate and fair pricing for insurance products, including price optimization in insurance. This approach allows insurers to better understand risk, enhance customer segmentation, and ultimately improve profitability. By leveraging data, insurers can create more personalized offerings and adjust premiums based on individual risk profiles, as seen in allstate price optimization.

4.1. Big Data in Insurance Pricing

Big data plays a crucial role in transforming how insurance pricing is approached, particularly in auto insurance price optimization. It enables insurers to analyze vast amounts of information from various sources, leading to more informed decision-making. The integration of big data into insurance pricing has several benefits:

- Enhanced risk assessment: Insurers can evaluate risks more accurately by analyzing diverse data points.

- Improved customer segmentation: Big data allows for more precise targeting of customer segments based on behavior and preferences.

- Dynamic pricing models: Insurers can adjust premiums in real-time based on changing risk factors and market conditions, which is essential for effective naic price optimization.

The use of big data in insurance pricing is becoming increasingly prevalent, with many companies investing in technology and analytics capabilities to stay competitive. At Rapid Innovation, we specialize in implementing AI-driven analytics solutions that empower insurers to harness big data effectively, leading to greater ROI through optimized pricing strategies, including insurance pricing optimization.

4.1.1. Key Data Sources and Collection

To effectively utilize big data in insurance pricing, insurers must identify and collect relevant data from various sources. Key data sources include:

- Internal data:

- Historical claims data

- Customer demographics

- Policyholder behavior and interactions

- External data:

- Social media activity

- Economic indicators

- Weather patterns and natural disaster data

- Third-party data providers:

- Credit scores

- Driving records

- Health and lifestyle information

Data collection methods can vary, but common techniques include:

- Surveys and questionnaires: Gathering information directly from customers about their preferences and behaviors.

- IoT devices: Using connected devices (e.g., telematics in cars) to collect real-time data on usage and behavior.

- Public records: Accessing government databases for information on property values, criminal records, and more.

By leveraging these data sources, insurers can create a comprehensive view of risk and tailor their pricing strategies accordingly. This data-driven approach not only enhances accuracy but also fosters trust and transparency with customers. Rapid Innovation's expertise in AI and big data analytics ensures that our clients can implement these strategies effectively, driving improved profitability and customer satisfaction. For more insights on the importance of data quality in AI implementations.

4.1.2. Real-Time Data Processing

Real-time data processing refers to the immediate processing of data as it is generated or received. This capability is crucial for businesses that need to make quick decisions based on the latest information.

- Immediate insights: Organizations can analyze data as it comes in, allowing for timely decision-making. Rapid Innovation leverages advanced AI algorithms to provide clients with actionable insights in real-time, enhancing their operational efficiency. This includes techniques such as real time data analysis and real time data enrichment.

- Enhanced customer experience: Real-time processing enables businesses to respond to customer inquiries and actions instantly, improving satisfaction. By implementing real-time data solutions, Rapid Innovation helps clients create seamless customer interactions that foster loyalty through real time data integration.

- Competitive advantage: Companies that leverage real-time data can adapt faster than competitors, leading to better market positioning. Rapid Innovation empowers clients to stay ahead of the curve by utilizing real-time analytics to inform strategic decisions, including real time stream analytics.

- Technologies involved: Tools like Apache Kafka, Apache Flink, and Amazon Kinesis are commonly used for real-time data streaming and processing. Rapid Innovation's expertise in these technologies ensures that clients can effectively harness the power of real-time data, including kafka real time streaming and real time etl.

- Use cases: Industries such as finance, e-commerce, and healthcare benefit significantly from real-time data processing for fraud detection, inventory management, and patient monitoring. Rapid Innovation has successfully implemented real-time solutions across various sectors, including real time data ingestion and realtime data ingestion, driving significant ROI for our clients. Additionally, real time stream processing is utilized to enhance operational capabilities. For more insights on this topic, visit Revolutionizing Data Processing: The Future of Edge AI and Micro Data Centers.

4.1.3. Data Quality and Governance Challenges

Data quality and governance are critical for ensuring that data is accurate, consistent, and trustworthy. Poor data quality can lead to misguided decisions and operational inefficiencies.

- Data accuracy: Ensuring that data is correct and free from errors is essential for reliable analysis. Rapid Innovation employs AI-driven data validation techniques to enhance data accuracy for our clients.

- Consistency: Data should be uniform across different systems and platforms to avoid discrepancies. Our blockchain solutions help maintain data integrity and consistency across decentralized networks.

- Completeness: Incomplete data can lead to skewed insights and hinder decision-making processes. Rapid Innovation assists clients in establishing comprehensive data collection strategies to ensure completeness.

- Governance frameworks: Establishing clear policies and procedures for data management helps maintain quality and compliance. Rapid Innovation collaborates with clients to develop robust governance frameworks tailored to their specific needs.

- Challenges faced: Organizations often struggle with data silos, lack of standardization, and insufficient resources for data governance. Rapid Innovation addresses these challenges by implementing integrated data solutions that break down silos and promote standardization.

- Impact of poor data quality: According to a study, poor data quality can cost organizations an average of $15 million per year (source: IBM). Rapid Innovation's focus on data quality and governance helps clients mitigate these costs and improve their bottom line.

4.2. Customer Segmentation and Personalization

Customer segmentation and personalization involve dividing a customer base into distinct groups and tailoring marketing efforts to meet the specific needs of each segment.

- Importance of segmentation: This process helps businesses understand diverse customer needs and preferences, leading to more effective marketing strategies. Rapid Innovation utilizes AI-driven analytics to provide clients with deep insights into their customer segments.

- Types of segmentation:

- Demographic: Based on age, gender, income, etc.

- Geographic: Based on location and regional preferences.

- Behavioral: Based on purchasing habits and product usage.

- Psychographic: Based on lifestyle, values, and interests.

- Personalization strategies: Utilizing data analytics to create personalized experiences, such as targeted emails, product recommendations, and customized content. Rapid Innovation helps clients implement these strategies to enhance customer engagement.

- Benefits of personalization:

- Increased customer engagement: Personalized experiences lead to higher interaction rates.

- Improved conversion rates: Tailored marketing messages can significantly boost sales.

- Enhanced customer loyalty: Customers are more likely to return to brands that understand their preferences.

- Tools and technologies: Customer Relationship Management (CRM) systems, data analytics platforms, and machine learning algorithms are commonly used to facilitate segmentation and personalization efforts. Rapid Innovation's expertise in these tools ensures that clients can effectively engage their customers and drive growth.

4.2.1. Microsegmentation for Tailored Pricing

Microsegmentation is a marketing strategy that involves dividing a customer base into smaller, more specific segments based on various criteria. This approach allows businesses to create microsegmentation pricing strategies that resonate with individual customer needs and preferences.

- Focus on specific demographics: Age, gender, income level, and location can all influence purchasing behavior.

- Behavioral data analysis: Analyzing past purchase behavior helps identify patterns and preferences.

- Personalized offers: Tailored pricing can include discounts, loyalty rewards, or exclusive deals for specific segments.

- Enhanced customer experience: By addressing the unique needs of each microsegment, businesses can improve customer satisfaction and loyalty.

- Increased revenue potential: Targeted pricing strategies can lead to higher conversion rates and increased sales.

At Rapid Innovation, we leverage AI algorithms to analyze vast datasets, enabling our clients to implement effective microsegmentation pricing strategies. By utilizing machine learning models, we help businesses identify and target specific customer segments, ultimately driving greater ROI through personalized marketing efforts.

4.2.2. Behavioral Scoring Models

Behavioral scoring models are analytical tools used to evaluate and predict customer behavior based on historical data. These models help businesses understand how likely a customer is to engage with a product or service, allowing for more effective marketing strategies.

- Data collection: Gather data from various sources, including purchase history, website interactions, and customer feedback.

- Scoring criteria: Develop criteria to score customers based on their likelihood to purchase, churn, or respond to marketing efforts.

- Predictive analytics: Use statistical techniques to forecast future behavior based on past actions.

- Segmentation: Classify customers into different groups based on their scores, enabling targeted marketing campaigns.

- Continuous improvement: Regularly update scoring models with new data to enhance accuracy and effectiveness.

Rapid Innovation employs advanced AI-driven behavioral scoring models to help clients predict customer actions with high precision. By integrating these models into their marketing strategies, businesses can optimize their campaigns, leading to improved customer engagement and increased sales.

4.2.3. Lifestyle-Based Pricing Factors

Lifestyle-based pricing factors consider the lifestyle choices and preferences of customers when determining pricing strategies. This approach recognizes that customers' lifestyles can significantly influence their purchasing decisions.

- Understanding customer lifestyles: Analyze factors such as hobbies, interests, and values to gain insights into customer behavior.

- Pricing tiers: Create different pricing tiers that cater to various lifestyle segments, such as budget-conscious consumers or luxury buyers.

- Value proposition: Align pricing with the perceived value of products or services based on lifestyle preferences.

- Marketing alignment: Tailor marketing messages to resonate with specific lifestyle segments, enhancing engagement and conversion rates.

- Flexibility in pricing: Offer customizable pricing options that allow customers to choose features or services that align with their lifestyle needs.

At Rapid Innovation, we utilize blockchain technology to ensure transparent and secure transactions for lifestyle-based pricing models. By implementing smart contracts, businesses can offer flexible pricing options that adapt to customer preferences, enhancing the overall customer experience and driving higher revenue.

4.2.4. Customized Coverage Recommendations

Customized coverage recommendations are essential for tailoring insurance products to meet the unique needs of individual clients, including custom equipment insurance and customized insurance coverage. This approach enhances customer satisfaction and retention by ensuring that clients receive the most relevant coverage options.

- Understanding Client Needs:

- Conduct thorough assessments of clients' personal or business circumstances.

- Utilize questionnaires or interviews to gather detailed information.

- Data-Driven Insights:

- Leverage data analytics to identify trends and patterns in client behavior.

- Use historical claims data to predict future coverage needs.

- Personalized Recommendations:

- Create tailored insurance packages based on the collected data.

- Offer options that align with clients' risk profiles and financial situations.

- Continuous Review and Adjustment:

- Regularly revisit and update coverage recommendations as clients' needs evolve.

- Implement feedback mechanisms to gauge client satisfaction and adjust offerings accordingly.

- Technology Utilization:

- Employ software tools that can analyze client data and generate customized recommendations.

- Use machine learning algorithms to enhance the accuracy of coverage suggestions.

5. Implementation Strategies and Best Practices

Implementing effective strategies and best practices is crucial for the successful deployment of customized coverage recommendations. These strategies ensure that the recommendations are not only relevant but also actionable.

- Clear Communication:

- Establish open lines of communication with clients to explain coverage options.

- Use simple language to ensure clients understand their choices.

- Training and Development:

- Invest in training programs for staff to enhance their understanding of customized coverage.

- Encourage continuous learning to keep up with industry trends and technologies.

- Client Engagement:

- Foster strong relationships with clients through regular check-ins and updates.

- Use surveys and feedback forms to gather insights on client experiences.

- Technology Integration:

- Implement customer relationship management (CRM) systems to track client interactions.

- Utilize digital platforms for easy access to policy information and recommendations.

- Performance Metrics:

- Establish key performance indicators (KPIs) to measure the effectiveness of coverage recommendations.

- Regularly analyze data to identify areas for improvement.

5.1. Integrating AI Technology

Integrating AI technology into the insurance industry can significantly enhance the process of providing customized coverage recommendations. AI can streamline operations, improve accuracy, and offer deeper insights into client needs.

- Enhanced Data Analysis:

- AI algorithms can process vast amounts of data quickly, identifying trends that may not be apparent to human analysts.

- Predictive analytics can forecast future client needs based on historical data.

- Personalization at Scale:

- AI can automate the customization process, allowing insurers to offer personalized recommendations to a larger client base.

- Machine learning models can adapt to new data, continuously improving the relevance of recommendations.

- Improved Customer Experience:

- Chatbots powered by AI can provide instant responses to client inquiries, enhancing engagement.

- AI-driven tools can guide clients through the coverage selection process, making it more intuitive.

- Risk Assessment:

- AI can analyze risk factors more accurately, leading to better underwriting decisions.

- This technology can help insurers identify high-risk clients and tailor coverage accordingly.

- Cost Efficiency:

- Automating routine tasks with AI can reduce operational costs and free up staff for more complex client interactions.

- AI can help identify fraudulent claims, saving insurers money in the long run.

At Rapid Innovation, we leverage our expertise in AI and blockchain technology to help clients implement these strategies effectively. By utilizing advanced data analytics and machine learning, we enable insurers to enhance their coverage recommendations, including custom equipment insurance and customized insurance coverage, ultimately driving greater ROI and improving client satisfaction. Our tailored solutions ensure that businesses can adapt to changing market dynamics while maintaining a competitive edge.

5.1.1. System Requirements and Readiness

System requirements refer to the necessary hardware and software specifications needed to run a particular application or system effectively. Assessing system readiness involves evaluating whether the current infrastructure can support the new system. Key considerations include:

- Hardware Specifications: Ensure that servers, workstations, and network devices meet the minimum requirements for processing power, memory, and storage.

- Software Compatibility: Verify that the operating systems and other software applications are compatible with the new system.

- Network Capacity: Evaluate bandwidth and latency to ensure that the network can handle the increased load from the new system.

- User Training: Assess the need for training programs to prepare users for the new system, ensuring they are familiar with its features and functionalities.

- Security Measures: Review existing security protocols to ensure they align with the requirements of the new system, including firewalls, antivirus software, and data encryption.

Conducting a system requirements assessment can help identify potential gaps and areas that need improvement before implementation. At Rapid Innovation, we leverage our expertise in AI and Blockchain to conduct thorough assessments, ensuring that your systems are primed for optimal performance and security.

5.1.2. Legacy System Compatibility

Legacy systems are older software or hardware that may still be in use but can pose challenges when integrating with new technologies. Compatibility issues can arise due to:

- Data Formats: Legacy systems may use outdated data formats that are not easily transferable to modern systems.

- APIs and Integration: Older systems may lack APIs or have limited integration capabilities, making it difficult to connect with new applications.

- Performance Limitations: Legacy systems may not have the processing power or speed required to support new functionalities.

Strategies for addressing compatibility include:

- Data Migration: Plan for data migration strategies that convert legacy data into formats compatible with the new system.

- Wrapper Solutions: Use middleware or wrapper solutions that allow legacy systems to communicate with new applications without requiring complete overhauls.

- Phased Approach: Implement a phased approach to gradually replace or upgrade legacy systems, minimizing disruption to business operations.

Understanding the implications of legacy system compatibility is crucial for ensuring a smooth transition to new technologies. Rapid Innovation specializes in creating tailored solutions that facilitate seamless integration, ensuring that your legacy systems can coexist with modern applications, thereby maximizing your ROI.

5.1.3. Cloud Deployment and Scalability

Cloud deployment refers to hosting applications and services on cloud infrastructure rather than on-premises servers. Benefits of cloud deployment include:

- Cost Efficiency: Reduces the need for significant upfront capital investment in hardware and maintenance.

- Accessibility: Enables remote access to applications and data from anywhere with an internet connection.

- Automatic Updates: Cloud providers often handle software updates and maintenance, ensuring systems are up-to-date.

Scalability is a key advantage of cloud deployment:

- On-Demand Resources: Organizations can easily scale resources up or down based on demand, allowing for flexibility in operations.

- Load Balancing: Cloud services can distribute workloads across multiple servers, enhancing performance and reliability.

- Global Reach: Cloud providers often have data centers in multiple locations, allowing businesses to expand their reach without significant infrastructure investment.

Considerations for cloud deployment include:

- Vendor Selection: Choose a reputable cloud provider that meets security, compliance, and performance requirements.

- Data Security: Implement robust security measures to protect sensitive data stored in the cloud.

- Cost Management: Monitor usage and costs to avoid unexpected expenses associated with cloud services.

Embracing cloud deployment and scalability can significantly enhance an organization's operational efficiency and responsiveness to market changes. At Rapid Innovation, we guide our clients through the cloud adoption process, ensuring that they leverage the full potential of cloud technologies to achieve greater ROI and operational agility.

5.1.4. API and Ecosystem Development

API (Application Programming Interface) and ecosystem development are crucial for enhancing the functionality and interoperability of software applications. APIs allow different software systems to communicate and share data seamlessly, such as through the google maps developer api or the shopify api developer.

- Facilitates integration: APIs enable various applications to work together, enhancing user experience. They allow businesses to connect with third-party services, such as the ebay api developer, expanding their capabilities and driving greater ROI through streamlined operations.

- Promotes innovation: Developers can create new applications or features by leveraging existing APIs, like the fastapi py framework. This fosters a culture of innovation, as businesses can quickly adapt to market changes, ensuring they remain competitive and responsive to customer needs.

- Enhances scalability: APIs allow businesses to scale their operations without overhauling existing systems. They can add new functionalities or services as needed, such as through api development or building apis, ensuring long-term growth and the ability to meet increasing demand efficiently.

- Supports data sharing: APIs facilitate the exchange of data between systems, improving decision-making. This is particularly important in industries like healthcare, finance, and e-commerce, where timely and accurate data is critical for operational success, as seen with the workday developer api.

- Encourages collaboration: An open API ecosystem invites developers to contribute, leading to a richer set of tools and services. Collaboration can lead to improved products and services, benefiting end-users and enhancing overall business performance, as demonstrated by the twitter developer site and the application programming interfaces available for various apps. For more insights on real-world AI implementations.

5.2. Change Management and Training

Change management is essential for organizations undergoing transformation, especially when implementing new technologies. Effective change management ensures that employees are prepared and supported throughout the transition.

- Establishes a clear vision: Communicating the purpose and benefits of the change helps align employees with organizational goals. A clear vision reduces resistance and fosters a positive attitude toward change, ultimately leading to a smoother transition.

- Involves stakeholders: Engaging employees in the change process encourages buy-in and reduces anxiety. Stakeholder involvement can provide valuable insights and feedback, ensuring that the change initiative is well-received and effectively implemented.

- Provides support systems: Offering resources such as help desks or mentorship programs can ease the transition. Support systems help employees navigate challenges and build confidence, which is essential for successful adoption of new technologies.

- Monitors progress: Regularly assessing the change process allows organizations to identify areas for improvement. Feedback loops can help refine strategies and ensure successful implementation, ultimately driving better outcomes.

- Celebrates milestones: Recognizing achievements during the change process boosts morale and motivation. Celebrating milestones reinforces the positive aspects of the transition, encouraging continued engagement and commitment from employees.

5.2.1. Employee Training for AI Tools

Training employees to use AI tools is vital for maximizing their potential and ensuring successful adoption. Proper training equips employees with the skills needed to leverage AI effectively.

- Identifies training needs: Assessing the current skill levels of employees helps tailor training programs. Understanding specific needs ensures that training is relevant and effective, leading to higher productivity and better utilization of AI resources.

- Offers hands-on experience: Practical training sessions allow employees to interact with AI tools directly. Hands-on experience builds confidence and familiarity with the technology, enabling employees to apply their knowledge in real-world scenarios.

- Provides ongoing support: Continuous learning opportunities help employees stay updated on AI advancements. Ongoing support fosters a culture of learning and adaptation, ensuring that the organization remains at the forefront of technological innovation.

- Encourages collaboration: Group training sessions promote teamwork and knowledge sharing. Collaborative learning can lead to innovative uses of AI tools, driving further efficiencies and enhancing overall business performance.

- Measures effectiveness: Evaluating training outcomes helps organizations understand the impact of their programs. Feedback from employees can guide future training initiatives and improvements, ensuring that the organization continues to evolve and adapt in a rapidly changing landscape.

5.2.2. Customer Communication Strategies

Effective customer communication is essential for building strong relationships and ensuring customer satisfaction. Here are key strategies to enhance communication: