1. Introduction

In the digital age, the financial sector has experienced tremendous growth and transformation, largely driven by advancements in technology. This evolution has not only expanded the services available to consumers but has also introduced complex challenges, notably in the realm of security. As financial transactions shift online, the potential for fraud has escalated, necessitating robust mechanisms for detection and prevention. Financial institutions and businesses are increasingly turning to sophisticated technologies to safeguard their operations and protect consumers from potential threats.

The importance of implementing effective fraud detection and prevention strategies cannot be overstated. These measures are crucial not only for protecting financial assets but also for maintaining customer trust and compliance with regulatory requirements. By understanding the various tools and techniques available for combating fraud, businesses can better prepare themselves against the ever-evolving tactics of fraudsters.

2. Fraud Detection and Prevention

Fraud detection and prevention are critical components of modern financial security frameworks. With the increasing volume of transactions and the sophistication of fraudulent schemes, it is essential for businesses to deploy advanced solutions that can identify and mitigate risks promptly. The goal of fraud prevention is not just to detect fraudulent activity after it has occurred but to prevent it from happening in the first place.

Technological advancements have paved the way for the development of various fraud detection tools and techniques. These include machine learning models that analyze patterns and behaviors, blockchain technology for secure and transparent record-keeping, and biometric verification systems that add an extra layer of security. Each of these technologies plays a pivotal role in the continuous fight against fraud, helping businesses stay one step ahead of fraudsters.

2.1. Real-time Transaction Monitoring

Real-time transaction monitoring is a vital aspect of fraud detection that allows businesses and financial institutions to analyze and assess transactions as they occur. This immediate scrutiny is crucial in identifying and responding to suspicious activities swiftly, thereby minimizing the risk of financial loss. Real-time monitoring systems utilize complex algorithms and machine learning techniques to flag anomalies that deviate from typical transaction patterns.

This technology not only helps in detecting fraudulent transactions but also plays a significant role in preventing them. By setting up real-time alerts, companies can quickly freeze suspicious transactions before they are processed, significantly reducing the incidence of fraud. Additionally, real-time data analysis provides valuable insights into consumer behavior, which can be used to enhance security measures and improve customer service.

For further reading on real-time transaction monitoring, you can explore resources from sources like Finextra or the Financial Times, which regularly publish articles on the latest developments in financial technology and its applications in fraud prevention.

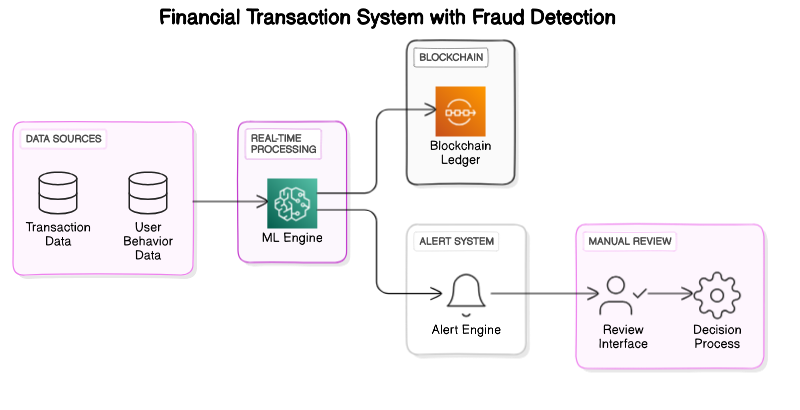

This architectural diagram illustrates the integration of various technologies within a financial transaction system to effectively detect and prevent fraud, providing a clear visual representation of the mechanisms discussed in the blog.

2.2. Predictive Analytics for Fraud Patterns

Predictive analytics is revolutionizing the way businesses detect and prevent fraud. By analyzing patterns and trends from vast amounts of data, predictive analytics can identify potential fraudulent activities before they occur. This proactive approach is particularly valuable in sectors like banking, insurance, and e-commerce, where fraud can have significant financial implications.

For instance, predictive models use historical data to recognize anomalies that deviate from normal behavior patterns. Techniques such as machine learning algorithms can continuously learn and adapt to new fraudulent tactics. This dynamic approach helps companies stay one step ahead of fraudsters. A practical example of predictive analytics in action is the detection of credit card fraud, where unusual transactions, based on previous spending patterns, are flagged for further investigation.

Moreover, the integration of predictive analytics with other technologies enhances its effectiveness. For example, linking predictive analytics with real-time monitoring systems can help in immediate detection and response to fraudulent activities, thereby minimizing potential losses. Resources like SAS (Predictive Analytics) provide further insights into how predictive analytics is applied in fraud detection.

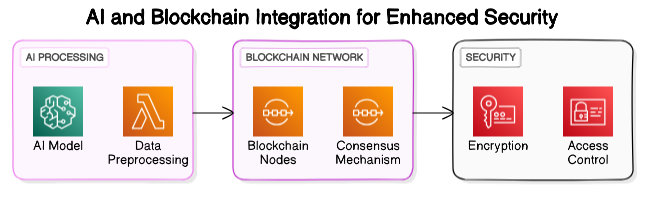

2.3. AI Integration with Blockchain for Enhanced Security

The integration of Artificial Intelligence (AI) with Blockchain technology promises a new level of security for digital transactions. Blockchain's decentralized nature makes it resistant to fraud, while AI can enhance this by quickly analyzing data blocks for any signs of tampering. This combination not only increases security but also improves the efficiency of operations.

AI algorithms can monitor and learn from the continuous flow of information on a blockchain, detecting anomalies that could indicate security breaches. For instance, in supply chain management, AI can help verify the authenticity of products by analyzing transaction blocks for discrepancies. This is crucial in combating counterfeiting and ensuring product integrity.

Furthermore, AI can automate complex processes involved in maintaining blockchain networks, such as optimizing data flow and validating transactions, which enhances the scalability of blockchain applications. The potential of AI in blockchain is explored in resources like IBM’s insights on blockchain and AI.

3. Customer Service Enhancement

AI technologies are significantly enhancing customer service across various industries. By integrating AI tools such as chatbots and virtual assistants, businesses are able to provide personalized, 24/7 support to their customers. These AI systems can handle a large volume of queries simultaneously, reducing wait times and improving customer satisfaction.

Chatbots, for example, are capable of learning from interactions with customers, which allows them to provide more accurate responses over time. They can also escalate complex issues to human representatives when necessary, ensuring that customers receive the level of support they need. This seamless integration of AI in customer service not only enhances efficiency but also helps in building stronger relationships with customers.

Moreover, AI-driven analytics can provide insights into customer preferences and behavior, enabling companies to tailor their services accordingly. This level of personalization is highly valued by customers and can significantly boost loyalty and retention. Insights into how AI is transforming customer service can be found on platforms like Salesforce.

Each of these points illustrates the transformative impact of technology in business, particularly through the lens of security and customer service enhancement.

3.1. Chatbots and Virtual Assistants

Chatbots and virtual assistants have revolutionized the way businesses interact with their customers. By leveraging artificial intelligence (AI) and natural language processing (NLP), these tools can simulate human-like conversations and provide instant responses to user inquiries. This technology not only enhances customer experience but also offers a scalable solution to handle large volumes of interactions without the need for extensive human resources.

The integration of chatbots and virtual assistants into customer service operations can significantly reduce operational costs and increase efficiency. Businesses can deploy these AI-driven tools across various platforms such as websites, social media, and mobile apps, ensuring a seamless customer service experience across all digital touchpoints. Moreover, advancements in AI continue to improve the responsiveness and accuracy of these tools, making them an indispensable asset for modern businesses.

3.1.1. Handling Customer Queries

Chatbots and virtual assistants are particularly effective in handling customer queries. They are programmed to understand and process user requests and can provide quick, accurate responses. This capability is crucial in today’s fast-paced world where customers expect immediate answers to their concerns. By automating responses to common inquiries, businesses can free up human agents to focus on more complex issues, thereby improving overall service quality.

These AI tools are also equipped with machine learning algorithms that allow them to learn from past interactions and improve over time. This means that the more they interact with users, the better they become at resolving queries. Additionally, they can handle multiple queries simultaneously, which significantly reduces wait times and enhances customer satisfaction.

3.1.2. Personalized Customer Interactions

One of the standout features of chatbots and virtual assistants is their ability to personalize interactions. By accessing and analyzing customer data, these tools can tailor their responses based on individual preferences and past behavior. This personalized approach not only makes the customer feel valued but also increases the relevance and effectiveness of the communication.

Personalization can extend from simple greetings and recommendations to more complex problem-solving scenarios. For instance, if a customer has a history of purchasing a particular product, the chatbot can offer related products or services, thereby enhancing the shopping experience and boosting sales. Furthermore, these tools can remember customer preferences and provide customized support during future interactions, which fosters loyalty and long-term engagement.

3.2. AI-Driven Customer Insights

AI-driven customer insights refer to the use of artificial intelligence technologies to analyze customer data and derive valuable insights that can help businesses understand their customers better and enhance their decision-making processes. AI tools can process vast amounts of data from various sources, including social media, customer reviews, and interaction logs, to identify patterns, trends, and customer preferences.

For instance, AI can be used to segment customers based on their behavior, preferences, and purchasing history, allowing companies to tailor their marketing strategies and product offerings more effectively. This level of personalization not only improves customer satisfaction but also boosts loyalty and revenue. AI-driven analytics can predict customer behavior, helping businesses to anticipate needs and offer solutions proactively.

Moreover, AI can enhance customer insights by integrating with other technologies such as machine learning and natural language processing. This integration allows for the automation of insight generation, reducing the time and effort required for data analysis and ensuring that the insights are both timely and relevant. For more detailed examples and case studies on AI-driven customer insights, you can visit sites like Forbes and TechCrunch (TechCrunch).

3.3. 24/7 Customer Support Automation

24/7 customer support automation involves using AI technologies, such as chatbots and virtual assistants, to provide constant support to customers without human intervention. This technology is particularly beneficial for handling common queries and issues, allowing human agents to focus on more complex customer needs. Automation tools can be integrated across various platforms, including websites, mobile apps, and social media, ensuring that customers receive immediate assistance regardless of the channel they use.

The use of AI in customer support not only enhances efficiency but also improves customer satisfaction by reducing wait times and providing consistent service quality. Automated systems can learn from interactions and improve over time, offering more accurate and helpful responses to customer inquiries. Additionally, they can handle multiple queries simultaneously, scaling as demand increases without the need for additional human resources.

For businesses looking to implement or improve their automated customer support systems, resources such as Zendesk (Zendesk) provide valuable insights and tools. These platforms offer solutions tailored to various business sizes and needs, helping companies to optimize their customer service operations effectively.

4. Risk Management

Risk management in the context of AI involves identifying, assessing, and mitigating risks associated with the deployment and operation of AI systems. This includes risks related to data privacy, security breaches, ethical concerns, and compliance with regulations. Effective risk management ensures that AI systems operate within legal and ethical boundaries and that they do not inadvertently harm users or other stakeholders.

AI can also be employed to enhance risk management strategies by predicting potential risks and suggesting mitigation strategies. For example, AI algorithms can analyze historical data to identify patterns that might indicate a security threat or a potential compliance issue, allowing organizations to address these risks proactively.

Furthermore, AI-driven risk management can lead to more informed decision-making, as it provides businesses with a comprehensive view of potential risks at an early stage. This proactive approach not only helps in minimizing potential damages but also in planning future strategies that align with both business objectives and regulatory requirements.

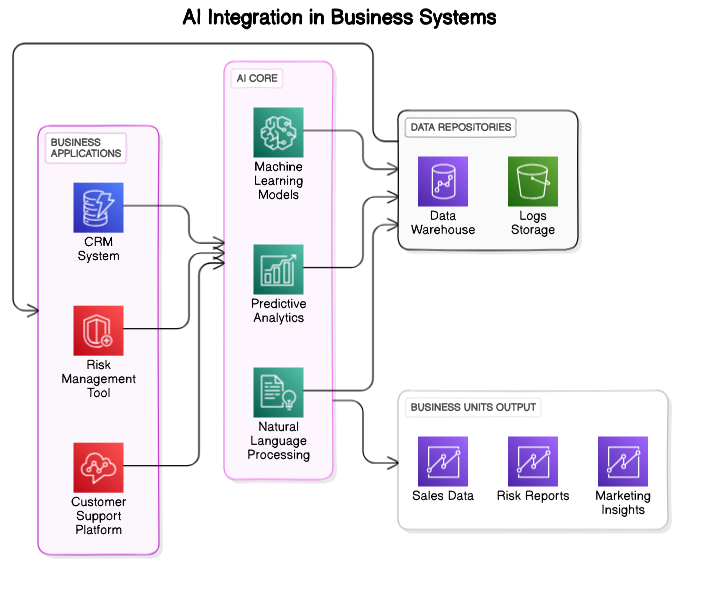

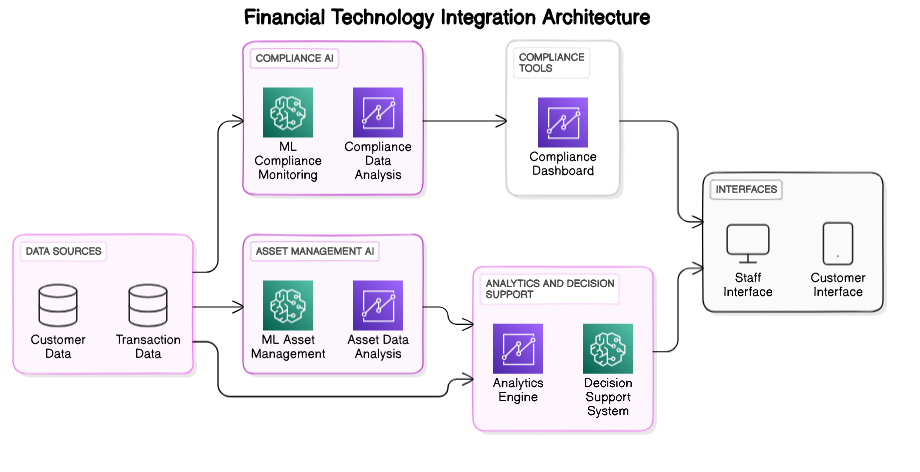

This architectural diagram illustrates the integration of AI technologies within business systems, showing how machine learning models, natural language processing, and predictive analytics work together with CRM, customer support platforms, and risk management tools to enhance business operations and decision-making processes.

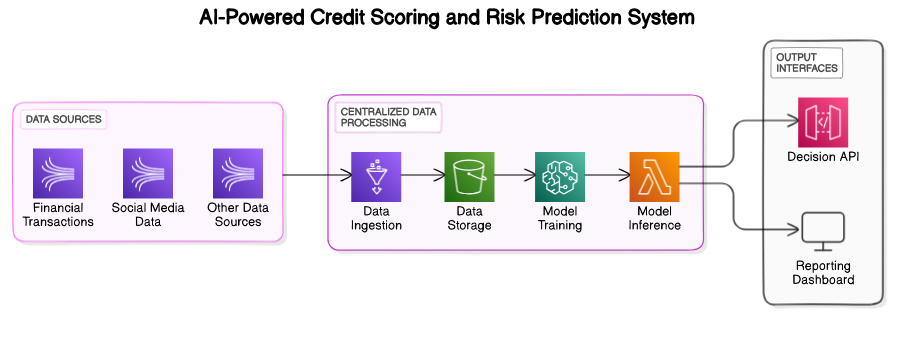

4.1. Credit Risk Assessment

Credit risk assessment is a crucial process in the financial sector, determining the likelihood that a borrower will default on their debt obligations. It involves evaluating the creditworthiness of potential borrowers, which helps financial institutions manage and mitigate potential losses. Traditional methods of credit risk assessment include manual review of financial statements, credit history, and other relevant financial data. However, with advancements in technology, this process has increasingly incorporated sophisticated analytical techniques and data-driven approaches.

The integration of big data analytics and machine learning has transformed credit risk assessment by enabling more accurate and dynamic risk evaluation. Financial institutions now leverage vast amounts of data, including non-traditional data sources such as social media activity and mobile phone usage patterns, to gain deeper insights into a borrower's behavior and financial stability. This data-driven approach allows for more personalized risk assessments and can lead to more inclusive credit practices, potentially lowering barriers for underserved populations.

4.1.1. AI Models for Credit Scoring

AI models for credit scoring represent a significant evolution in the methodology used to assess creditworthiness. These models utilize machine learning algorithms to analyze large datasets, identifying patterns and correlations that may not be evident through traditional analysis. By incorporating variables such as spending habits, the frequency of financial transactions, and even geographic data, AI can provide a more comprehensive view of a borrower's financial health.

One of the key advantages of using AI in credit scoring is its ability to continuously learn and adapt. As new data becomes available, AI models can update their predictions to reflect current economic conditions and trends. This results in more accurate and up-to-date credit scores, which are crucial for both lenders and borrowers in making informed financial decisions.

4.1.2. Risk Prediction Algorithms

Risk prediction algorithms are at the heart of modern credit risk assessment, providing tools that forecast the likelihood of a borrower defaulting. These algorithms analyze historical data and apply statistical techniques to predict future behavior based on established patterns. The sophistication of these models can vary significantly, from basic logistic regression models to complex neural networks.

The use of big data and machine learning has greatly enhanced the capabilities of risk prediction algorithms. By integrating diverse data sources, such as real-time economic indicators or even psychometric evaluations, lenders can obtain a nuanced understanding of risk that goes beyond traditional financial metrics. This holistic approach not only improves the accuracy of predictions but also helps in tailoring financial products to meet the specific needs of different customer segments.

For more detailed information on risk prediction algorithms, you can explore resources like the Harvard Business Review for discussions on their strategic implications, or delve into technical papers available through the IEEE Xplore digital library, which provide in-depth analyses of various algorithmic approaches used in risk prediction.

4.2. Asset Management

Asset management in the financial sector refers to the systematic process of developing, operating, maintaining, and selling assets in a cost-effective manner. For banks and financial institutions, effective asset management is crucial as it directly influences their ability to generate profits and ensure customer satisfaction. Asset management services range from investment management for individuals and institutions to managing a wide array of assets including stocks, bonds, real estate, and other investments.

One of the primary goals of asset management is to maximize returns while minimizing risk. This involves strategic asset allocation, thorough market analysis, and the implementation of advanced financial models and investment strategies. Financial advisors and asset managers play a key role in guiding clients through the complexities of investment options, tailored to their financial goals and risk tolerance.

Technological advancements have significantly transformed asset management. Digital tools and software solutions enable better portfolio management, real-time analytics, and enhanced decision-making processes. For instance, platforms like Bloomberg and Morningstar provide comprehensive analytics that help in making informed investment decisions. Moreover, the integration of artificial intelligence and machine learning has paved the way for more predictive and personalized asset management solutions, enhancing the overall efficiency and effectiveness of the services provided. Learn more about the transformation of investment advice through AI-powered Robo-Advisors.

4.3. Regulatory Compliance Monitoring

Regulatory compliance monitoring is a critical function for financial institutions, ensuring that they adhere to all laws, regulations, and guidelines applicable to their operations. This is vital not only to maintain legal and ethical standards but also to protect the interests of consumers and maintain the integrity of the financial system. Compliance involves various aspects such as anti-money laundering (AML), combating the financing of terrorism (CFT), and adhering to financial services regulations.

The complexity of regulatory frameworks means that banks must invest heavily in compliance programs. These programs involve continuous monitoring and auditing processes to detect and prevent violations and to ensure that the institution remains in good standing with regulators. The use of technology in compliance has grown significantly, with tools designed to automate and streamline the monitoring processes. For example, software solutions like Thomson Reuters CLEAR and LexisNexis Risk Solutions are widely used for their robust compliance tools and resources.

Moreover, the global nature of modern banking necessitates a comprehensive understanding of both local and international regulations. This is particularly challenging as rules can vary significantly across different jurisdictions. Continuous training and development programs for compliance officers are therefore essential to keep up with the ever-changing regulatory landscape.

5. Personalized Banking

Personalized banking represents a shift towards more customized financial services, tailored to meet the unique needs of each customer. This approach leverages data analytics and technology to offer personalized products, advice, and customer service. The aim is to enhance customer satisfaction, increase loyalty, and ultimately drive revenue growth.

Banks use various data points such as spending habits, income levels, and personal goals to create a more personalized banking experience. This can include customized banking advice, tailored investment solutions, and personalized loan and credit options. Technologies such as AI and machine learning play a crucial role in analyzing customer data and providing insights that help in delivering personalized services.

Moreover, personalized banking is not just about offering tailored products but also about providing a seamless customer experience across various channels. Whether it’s through mobile apps, online banking, or in-person services, ensuring a consistent and personalized experience is key to customer retention and satisfaction. For example, apps like Mint and Personal Capital help users manage their finances more effectively by providing personalized insights and budgeting tools.

In conclusion, personalized banking is becoming increasingly important in the competitive financial services industry. By focusing on individual customer needs and preferences, banks can differentiate themselves and foster stronger relationships with their clients.

5.1. AI in Wealth Management

Artificial Intelligence (AI) is revolutionizing the field of wealth management, offering sophisticated tools that enhance the capabilities of financial advisors and improve client outcomes. AI technologies, such as machine learning and predictive analytics, are being used to analyze vast amounts of data to identify investment opportunities and risks, thereby enabling more informed decision-making.

For instance, AI can process and analyze market data at a speed and accuracy that is impossible for human analysts. This capability allows wealth managers to react more quickly to market changes and tailor their strategies accordingly. Additionally, AI-driven tools can help in risk assessment by predicting market volatility and suggesting the optimal risk management strategies. This not only helps in maximizing returns but also in protecting investments during downturns.

Moreover, AI enhances client engagement and service in wealth management by providing personalized insights and recommendations based on individual client profiles. This level of customization improves client satisfaction and loyalty, which are crucial for the success of wealth management firms.

5.2. Personalized Financial Advice

Personalized financial advice has become increasingly important in a world where financial needs and situations vary greatly from one individual to another. AI and data analytics play a pivotal role in delivering customized advice that aligns with individual financial goals and risk tolerances. By leveraging data from various sources, AI algorithms can create detailed financial profiles and predict future needs, enabling advisors to offer tailored advice.

This personalized approach not only helps in building trust and rapport with clients but also enhances the effectiveness of financial planning. For example, AI can help identify the best investment opportunities for a client based on their past investment history, current financial status, and future goals. Additionally, it can provide scenario-based planning tools that help clients understand potential outcomes of different financial decisions.

The use of AI in providing personalized financial advice is a game-changer, particularly in complex financial markets. Clients benefit from receiving advice that is not only aligned with their financial goals but also responsive to market dynamics. For further reading, check out insights from Kiplinger and Investopedia, which discuss how AI is transforming personal financial advice.

5.3. Tailored Banking Products

Banks are increasingly using AI to develop tailored banking products that meet the unique needs of their customers. By analyzing customer data, AI can help banks understand individual behaviors and preferences, which can be used to design customized products such as loans, credit cards, and investment plans. This not only enhances customer satisfaction but also increases the likelihood of product uptake.

For example, AI can analyze a customer’s spending patterns, saving habits, and financial goals to offer a credit card with features that best suit their lifestyle, such as higher rewards in categories where they spend the most. Similarly, AI-driven insights can help banks offer personalized loan products with variable interest rates and repayment terms that match the borrower’s financial capacity.

The ability to offer tailored products not only gives banks a competitive edge but also plays a crucial role in customer retention. By addressing the specific needs of customers, banks can build stronger relationships and foster loyalty. For more information on how AI is used to tailor banking products, you can explore articles from American Banker and The Financial Brand, which provide comprehensive analyses of this trend.

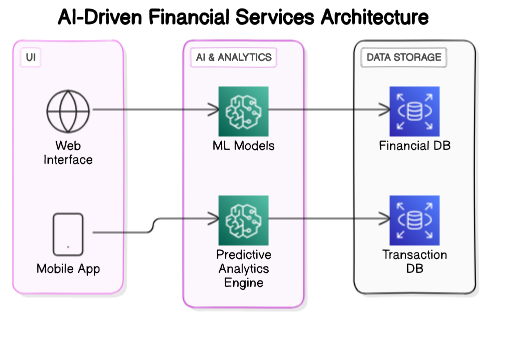

This architectural diagram illustrates the integration of AI technologies within financial services, showing how machine learning models, predictive analytics, and other AI components interact with financial databases and user interfaces to deliver personalized services and enhance decision-making processes.

6. Process Automation

Process automation has become a cornerstone in enhancing efficiency, reducing costs, and improving accuracy across various industries. By automating routine and repetitive tasks, businesses can allocate human resources to more strategic roles that require human insight and decision-making skills. Automation technologies, including software and robotics, are employed to perform tasks that were traditionally done by humans. This shift not only speeds up processes but also minimizes the risk of human error, leading to more consistent and reliable outcomes.

The implementation of process automation tools has been particularly transformative in sectors like manufacturing, banking, healthcare, and retail. These tools help streamline operations, from inventory management to customer service, ensuring that businesses can operate smoothly and scale effectively. As technology evolves, the scope of process automation continues to expand, offering new ways to enhance business operations and drive innovation.

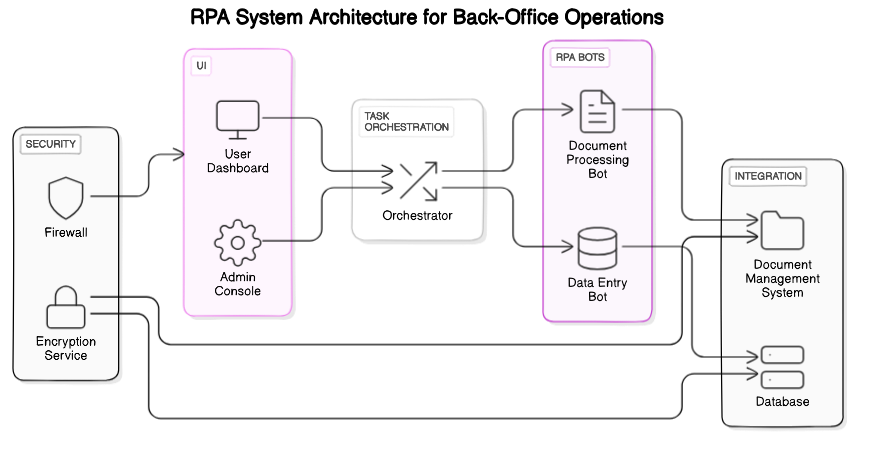

6.1. Robotic Process Automation in Back-Office Operations

Robotic Process Automation (RPA) is revolutionizing back-office operations, which are typically characterized by high-volume, repetitive tasks. RPA allows businesses to automate such tasks as data entry, processing transactions, and managing records. This not only speeds up the processes but also significantly reduces the likelihood of errors, ensuring higher accuracy and compliance with regulatory standards.

For example, in the financial sector, RPA can automate the reconciliation of accounts, processing of claims, and compliance reporting, which are time-consuming when performed manually. This automation leads to faster turnaround times and frees up employees to focus on more complex and customer-focused tasks. The adoption of RPA in back-office operations is not just about cost savings; it also enhances employee satisfaction by removing mundane tasks from their workload, allowing them to engage in more meaningful and rewarding work.

For further reading on RPA in back-office operations, you can visit sites like Automation Anywhere.

6.2. Document Verification and Processing

Document verification and processing is another area where automation is making significant inroads. Using technologies such as Optical Character Recognition (OCR) and Artificial Intelligence (AI), automated systems can quickly scan, verify, and process documents. This is particularly useful in industries like legal, banking, and real estate, where document verification is crucial and needs to be done quickly and accurately.

Automated document processing reduces the need for manual checking, which not only speeds up the process but also reduces the chances of human error. For instance, in mortgage processing, automation can verify the authenticity of documents, check for compliance, and even flag potential issues, all within a fraction of the time it would take a human to perform the same tasks. This not only accelerates the approval process but also enhances customer satisfaction by providing quicker services.

Moreover, automation in document processing ensures better data management and storage. Digital documents can be easily indexed and retrieved, making the management of large volumes of documents more manageable and less prone to errors. This is a significant advantage in any compliance-driven environment where document retention and accuracy are paramount.

For more insights into document verification and processing automation, consider exploring resources available on ABBYY or Kofax. Additionally, read about the influence of RPA on legal document review on Rapid Innovation's blog.

6.3. AI in KYC and Anti-Money Laundering

The integration of Artificial Intelligence (AI) in Know Your Customer (KYC) and Anti-Money Laundering (AML) processes is revolutionizing the financial sector by enhancing the efficiency and accuracy of compliance procedures. AI technologies, including machine learning and natural language processing, are being employed to streamline the identification and verification processes, detect suspicious activities, and reduce false positives.

AI-driven KYC solutions automate the data collection and verification process, making it faster and more accurate. By using AI, financial institutions can quickly analyze vast amounts of data, including public records and digital footprints, to authenticate identities and assess customer risk profiles. This automation not only speeds up the onboarding process but also helps in maintaining up-to-date customer information, which is crucial for compliance. For instance, tools like identity verification software can scan and authenticate various documents in real-time, significantly reducing human error and operational costs.

In the realm of AML, AI is instrumental in identifying patterns and anomalies that may indicate money laundering activities. Traditional methods of monitoring and reporting suspicious activities are often cumbersome and prone to errors. AI enhances these processes by continuously learning from transaction data, customer behavior, and previous investigations to improve detection accuracy. Advanced algorithms can sift through millions of transactions to spot complex patterns that would be impossible for human analysts to detect manually. This capability is crucial in combating sophisticated financial crimes that might otherwise go unnoticed.

Moreover, AI can also help in reducing false positives, which are a significant challenge in AML operations. False positives, or legitimate transactions that are wrongly flagged as suspicious, can lead to unnecessary investigations, wasting resources and time. AI systems can refine detection parameters over time, learning to distinguish between genuine and fraudulent activities more effectively.

For further reading on the impact of AI in KYC and AML, you can visit sites like Forbes for insights on AI advancements in financial sectors (Forbes), Finextra for detailed articles on technology in finance (Finextra), and the Financial Action Task Force (FATF) for guidelines and reports on money laundering and terrorist financing (FATF). These resources provide comprehensive information and expert opinions on the evolving role of AI in financial compliance.

7. Conclusion

The exploration of the topic at hand reveals a multifaceted landscape where various factors interplay to shape outcomes. Throughout the discussion, it becomes evident that understanding the nuances and complexities is crucial for a comprehensive grasp of the subject. This conclusion aims to encapsulate the key insights and forward-looking perspectives that emerged from the analysis.

Firstly, the importance of data-driven decision-making has been underscored repeatedly. In an era where information is abundant, leveraging accurate data to guide choices stands out as a fundamental strategy for success. Whether in business, healthcare, or technology, the integration of robust data analytics proves to be a decisive factor in enhancing efficiency and effectiveness. For further reading on the impact of data in decision-making processes, resources such as Forbes and Harvard Business Review offer extensive analyses and case studies.

Secondly, the role of innovation in driving progress cannot be overstated. As discussed, continuous innovation not only addresses current needs but also anticipates future challenges, thereby securing a competitive edge. This is particularly visible in sectors like technology and sustainability, where innovation leads to breakthroughs that redefine market standards and consumer expectations. Websites like TechCrunch and WIRED provide ongoing coverage of the latest innovations across various industries.

Lastly, the discussion highlighted the significance of adaptability and resilience. In a rapidly changing world, the ability to adapt and respond to new challenges is crucial for survival and growth. This trait is essential not just for individuals but also for organizations and societies. Insights into developing resilience can be explored through educational resources and professional publications such as Psychology Today and the American Psychological Association.

In conclusion, while the landscape is complex and challenges are inevitable, the pathways to overcoming them are clear: informed decision-making, relentless innovation, and robust adaptability. These elements are not only essential for tackling current issues but also for paving the way for future success.

.svg)